2026 Denver Metro Renewal Wave: Strategic Refinancing Moves to Save $300 to $600 a Month

Navigating Maturing Low-Rate Loans in Centennial and Beyond

The Denver Metro housing market is approaching a significant milestone. As we look toward 2026, thousands of Colorado homeowners are facing the reality of maturing low-rate loans, shifting financial goals, and evolving family needs. If you secured a record-low mortgage rate a few years ago, you might feel locked into your current home. However, leveraging strategic refinancing moves could help you save anywhere from $300 to $600 per month.

At Choice Mortgage Group RJ Baxter Team, we specialize in helping homeowners in Centennial and the greater Denver area navigate these complex financial waters. Whether you are dealing with high-interest credit card debt or need to fund a major home renovation, understanding how to calculate blended rates is crucial. A blended rate combines your current low first mortgage rate with the cost of new borrowing, often revealing that a cash-out refinance is much more affordable than you might think.

- Evaluate your complete debt profile: Look beyond just your mortgage rate to see what you are paying overall across auto loans and credit cards.

- Consider a debt consolidation refinance: Paying off high-interest consumer debt can drastically lower your monthly cash outflow.

- Work with a local expert: Partnering with a Centennial mortgage lender ensures you get advice tailored specifically to the Colorado real estate market.

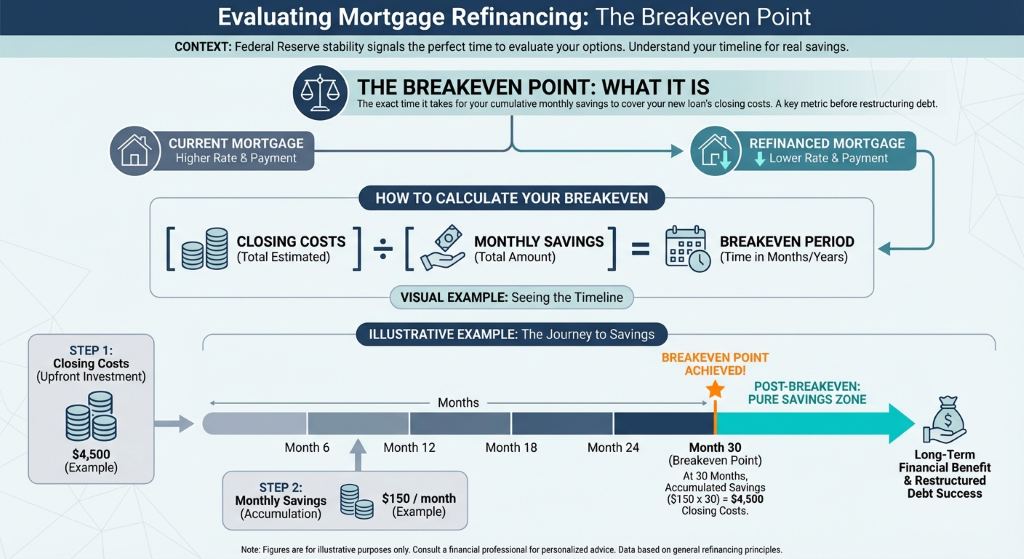

Calculating Your Breakeven Point Amid Fed Stability

With the Federal Reserve showing signs of stability, now is the perfect time to evaluate your refinancing options. One of the most important metrics to understand before restructuring your debt is your breakeven point. This is the exact amount of time it takes for your monthly savings to exceed the closing costs associated with your new mortgage loan.

To calculate your breakeven point, simply divide your total estimated closing costs by your total monthly savings. For example, if your refinance costs $3,000 and saves you $300 a month, your breakeven point is exactly 10 months. If you plan to stay in your Centennial home longer than those 10 months, refinancing is a highly sound financial strategy.

Timing the market perfectly is nearly impossible, but waiting for rates to drop further can sometimes cost you more in missed monthly savings. By analyzing your unique financial situation, our team can help you determine if acting now will protect your wealth and improve your monthly cash flow.

| Current Monthly Debt Payments | New Refinanced Payment | Monthly Savings | Breakeven Time (Months) |

|---|---|---|---|

| $3,500 | $3,200 | $300 | 12 |

| $4,100 | $3,650 | $450 | 9 |

| $4,800 | $4,200 | $600 | 7 |

Why Choose a Centennial Mortgage Lender for Your Refinance

Finding the right home loan requires careful consideration of your needs, finances, and history. When navigating the 2026 Denver Metro renewal wave, working with a local professional who understands the nuances of the Colorado market is invaluable. The RJ Baxter Team is known throughout the Denver marketplace for our high level of communication and dedicated follow-up.

We know you do not deal with mortgages every day like we do. That is why we use common sense and communicate with you in terminology that you will understand, completely avoiding complicated mortgage broker and real estate jargon. We treat every client like family and strive to give you the best possible, stress-free mortgage experience.

If you are wondering how much you qualify for or want to explore your loan options without any obligation or credit check, we are here to help. Our team specializes in market trends and helps homeowners determine the absolute best time to refinance to maximize their savings.

Q1: What is the 2026 Denver Metro renewal wave?

It refers to the upcoming period when many Colorado homeowners who secured low-rate adjustable or short-term loans years ago will need to reassess their mortgage strategies as those loan terms mature.

Q2: How does a blended rate work in a mortgage refinance?

A blended rate is the combined average interest rate of your existing low-rate mortgage and any new debt you take on. This calculation often proves that consolidating debt results in a lower overall cost than maintaining separate high-interest accounts.

Q3: How do I calculate my refinance breakeven point?

You calculate your breakeven point by dividing your total closing costs by your total monthly savings. This formula tells you exactly how many months it will take to recoup the upfront cost of refinancing.

Q4: Is it smart to refinance if I already have a low mortgage rate?

Yes, it can be very smart if you have accumulated high-interest consumer debt. A cash-out refinance can consolidate that debt, lowering your total monthly financial obligations significantly despite a slightly higher mortgage rate.

Q5: Why should I work with a local Centennial mortgage lender?

A local lender like the RJ Baxter Team understands the specific property values, market trends, and loan programs unique to Centennial and the broader Colorado market, ensuring you receive the most accurate and beneficial financial advice.Get Your Custom Refinance Quote Today