Condo and HOA-Heavy Properties in Colorado: Financing Strategies for 2026

Navigating Condo Approvals in Centennial and Highlands Ranch

As we look toward 2026, the suburban boom in Colorado continues to reshape the local housing market. In highly sought-after areas like Centennial and Highlands Ranch, homebuyers are increasingly turning to condos and townhomes to find affordable, low-maintenance living. However, financing a property within a Homeowners Association (HOA) involves more than just qualifying for a mortgage based on your personal income and credit score. The property itself must also be approved by the lender.

When you apply for a loan on a condo, lenders will classify the property as either warrantable or non-warrantable. A warrantable condo meets the strict guidelines set by government-backed entities like Fannie Mae, Freddie Mac, the FHA, or the VA. These guidelines ensure the community is financially stable and not overly dominated by investors. If a condo building fails to meet these criteria, securing traditional financing becomes much more difficult.

- Owner-Occupancy Ratios: Lenders typically prefer communities where the majority of units are owned by primary residents rather than investors.

- Commercial Space Limits: For a condo to be warrantable, the building usually cannot have more than 35 percent of its total space dedicated to commercial use.

- Single-Entity Ownership: Lenders will check to ensure that no single person or company owns more than 20 percent of the units in the development.

Working with a local expert like the RJ Baxter Team at RJ Baxter - NEO Home Loans is crucial. We understand the specific nuances of the Centennial and Highlands Ranch markets and can help you identify warrantable properties early in your search, saving you time and frustration.

Understanding HOA Reserve Requirements and Special Assessments

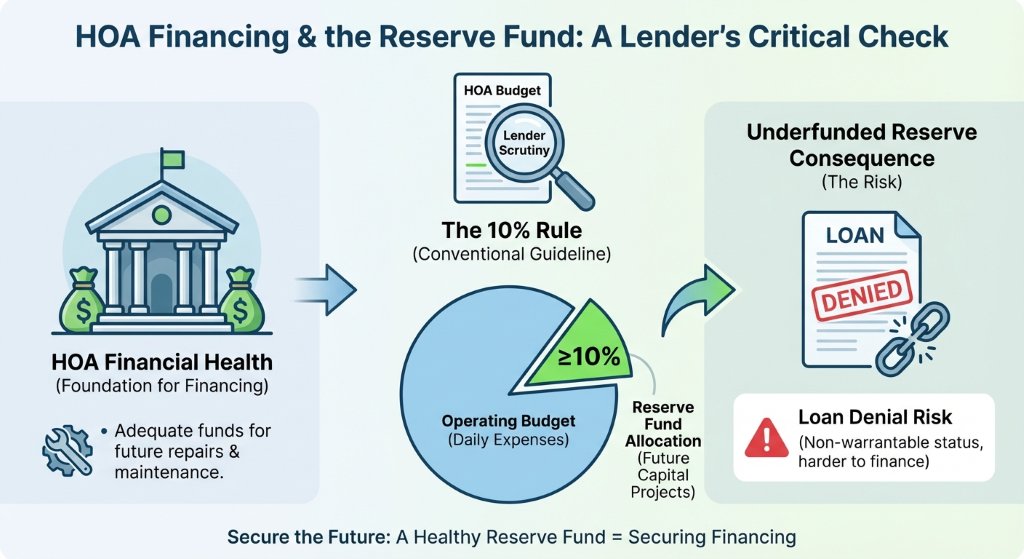

One of the most critical factors in securing financing for an HOA-heavy property is the financial health of the association itself. Lenders will closely scrutinize the HOA budget to ensure there are adequate funds set aside for future repairs and maintenance. This is known as the reserve fund.

For a condo to meet standard conventional lending guidelines, the HOA must allocate at least 10 percent of its annual operating budget to the reserve account. If the reserve fund is underfunded, the lender may view the property as too risky to finance. An underfunded HOA is a red flag because it often leads to deferred maintenance or sudden financial burdens on the homeowners.

When the reserve fund is insufficient to cover major repairs like a new roof or structural fixes, the HOA may issue a special assessment. A special assessment is an unexpected fee charged to homeowners on top of their regular monthly dues. Lenders are highly cautious of communities with pending or active special assessments. If an assessment is currently in place, the lender will need to verify that it will not negatively impact your ability to repay your mortgage.

To protect yourself as a buyer, you should always request and carefully review the HOA documents, including the reserve study, recent meeting minutes, and the current budget. The RJ Baxter Team can guide you through this documentation to ensure the community you choose is on solid financial footing.

| Condo Classification | Typical Financing Available | HOA Financial Requirements | Lender Risk Level |

|---|---|---|---|

| Warrantable | Conventional, FHA, VA | 10% minimum budget in reserves, no major litigation | Low Risk |

| Non-Warrantable | Portfolio Loans, Hard Money | May have underfunded reserves or pending lawsuits | High Risk |

| New Construction | Conventional (with presale limits) | Developer must transfer control properly | Moderate Risk |

How to Prepare for Your 2026 Colorado Condo Purchase

Buying a condo in Colorado’s competitive suburban markets requires a proactive strategy. The first step is to get fully pre-approved for a mortgage before you start touring properties. A pre-approval from a reputable local lender gives you a clear understanding of your budget and shows sellers that you are a serious, qualified buyer.

When calculating your purchasing power, remember to factor in the monthly HOA dues. These fees are included in your debt-to-income (DTI) ratio, which means higher HOA fees will reduce the maximum loan amount you can qualify for. It is essential to communicate openly with your lender about the specific communities you are targeting so they can run accurate payment scenarios.

- Partner with Local Experts: Choose a real estate agent and a mortgage lender who have extensive experience with condos in Centennial and Highlands Ranch.

- Ask About Pending Litigation: Lenders will not approve a loan if the HOA is involved in significant structural litigation. Always ask about lawsuits upfront.

- Review the Master Insurance Policy: Ensure the HOA carries sufficient hazard and liability insurance, as lenders will require proof of this coverage before closing.

At RJ Baxter - NEO Home Loans, RJ Baxter and his team pride themselves on high-level communication and a stress-free loan process. We treat every client like family and use our deep knowledge of the Colorado market to help you navigate the complexities of condo financing.

Q1: What is a warrantable condo in Colorado?

A warrantable condo is a property that meets the lending guidelines set by Fannie Mae, Freddie Mac, FHA, or VA. This means the HOA is financially stable, has adequate reserves, and the building is primarily owner-occupied rather than dominated by investors.

Q2: How do HOA fees affect my mortgage qualification?

HOA fees are factored into your debt-to-income (DTI) ratio. Because they are considered a recurring monthly debt, higher HOA fees will lower the total mortgage amount you can qualify for.

Q3: What happens if a condo community has a special assessment?

If there is an active special assessment, the lender will review the reason for the assessment and the financial impact on the unit. If the assessment threatens the structural integrity of the building or your ability to make payments, it could delay or prevent loan approval.

Q4: Why do mortgage lenders care about HOA reserve funds?

Lenders want to ensure the HOA has enough money saved for major future repairs. If reserves are too low, the property could fall into disrepair, lowering its value and increasing the risk for the lender.

Q5: Can I get a loan for a non-warrantable condo in Centennial?

Yes, but it is more challenging. You will typically need a specialized portfolio loan rather than a standard conventional mortgage. These loans often require a larger down payment and may come with higher interest rates.Contact RJ Baxter at RJ Baxter - NEO Home Loans Today to Start Your Pre-Approval